We looked at PC manufacturers in the fall. Since we last talked, economic sentiment has changed tremendously. Here is an update on how the three big manufacturers are doing. From SeekingAlpha.com

U.S. consumers and businesses aren’t buying PCs like they used to – and the economic slowdown continues to take a big bite out of personal computer demand.

Two recent ChangeWave surveys focused on PC purchasing trends among consumers and corporations. The results clearly show deteriorating PC spending going forward.

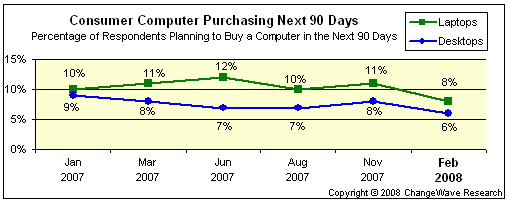

Next 90 Days: PCs Head South

Consumers. Only 8% of the 4,427 consumers surveyed by ChangeWave in late February say they’ll be buying a laptop in the next 90 days – down 3-percentage points since November 2007. Most importantly, that’s a record low for the past 12 months.

The same trend was found for desktops, with just 6% saying they’ll be buying a one – also a low for the year.

Graph

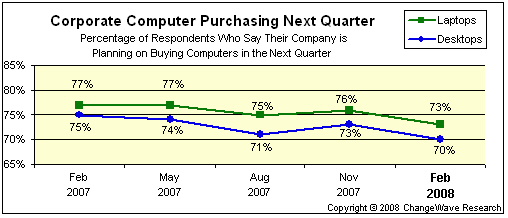

Businesses. In a double whammy, corporate PC buying has also slowed precipitously. In February, only 73% of 2,204 corporate respondents said their company plans on buying laptops in the next quarter – down 4-pts from a year ago. It’s the same pattern for desktops, with corporate purchases down 5-pts.

Graph

But what impact, if any, is the PC slowdown having on major manufacturers? Let’s look at three of the heavyweights:

Apple Mac Sales Remain Relatively Strong

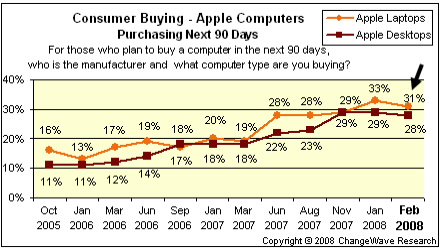

Planned purchases of Apple (AAPL) computers remain relatively strong even in the slower PC buying environment.

Looking at the next 90 days, Apple remains the leader among consumers who plan to buy a laptop (31%) – down just 2-pts from the all-time high recorded in our previous survey. Apple planned desktop purchases (28%; down 1-pt) are also near record levels.

Graph

Importantly, Apple’s planned buying numbers are up more than 50% from a year ago.

In the corporate market, planned Mac purchases for next quarter are also at near record highs, with laptops (7%) unchanged from previously and desktops (6%) down just 1-pt.

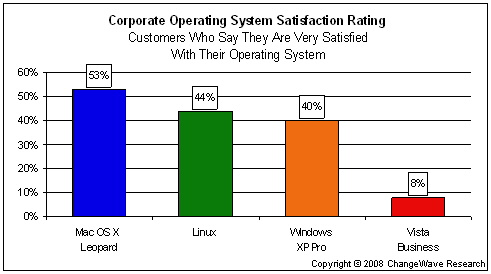

Most positively for Apple, the company continues to set the standard for customer satisfaction. Among corporate respondents using the Leopard operating system, better than half (53%) report they are Very Satisfied.

This compares to a 40% Very Satisfied rating for Windows XP Pro users, and a miniscule 8% Very Satisfied rating for Microsoft (MSFT) Vista Business (8%).

Graph

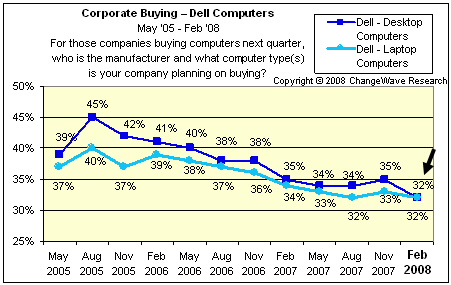

Another Ebb for Dell

In contrast to Apple, we find a far different story with Dell (DELL).

After experiencing a tiny uptick in planned consumer buying in our previous survey, Dell is once again losing traction going forward. Planned purchases of Dell laptops (28%; down 2-pts) and especially desktops (32%; down 4-pts) are considerably weaker than in our previous survey.

Dell is also plagued by a downturn in planned corporate buying for next quarter, with desktop (32%; down 3-pts) and laptop (32%; down 1-pt) purchases falling to new lows.

Graph

“It’s like déjà vu, all over again,” Yogi Berra famously said, and that’s what it looks like as Dell once again resumes its market share slide.

Weakening Sales for Hewlett-Packard

Another major player, Hewlett-Packard (HPQ), also exhibits weaker PC sales going forward – led by a big drop in consumer planned buying of desktops (18%; down 5-pts) and laptops (19%; down 2-pts).

In terms of corporate planned purchases, H-P also look weaker going forward, both for desktops (17%; down 1-pt) and laptops (14%; down 2-pts).

Hewlett-Packard recently announced strong computer sales. But almost 70% of its sales come from outside the U.S. – where the current slowdown is likely having less of an impact – while our ChangeWave surveys focus mainly on the U.S. market.

Indeed, outside the U.S., H-P registers higher market share numbers for consumer desktops (22%), corporate desktops (20%) and corporate laptops (17%).

Nonetheless, weaker U.S. visibility clearly looks to be an issue for Hewlett-Packard going forward.

Jim Woods co-wrote this article.

Sunday, March 30, 2008

Update on PC Market

Tuesday, March 25, 2008

Luck, Deception and Incentives in Finance

From Martin Wolf at FT.com

Hardly a week goes by without the implosion of a hedge fund. Last week it was Carlyle Capital, with an astonishing $31 of debt for each dollar of equity. But we should not be surprised. These collapses are inherent in the hedge-fund model. It is even conceivable that this model will join securitised subprime mortgages on the scrap heap.

Getting away with producing adulterated milk is hard; getting away with an investment strategy that adds no value is not. That was the point made by John Kay, in a superb column last week (this page, March 11). With the “right” fee structure mediocre investment managers may become rich as they ensure that their investors cease to remain so.

Two distinguished academics, Dean Foster at the Wharton School of the University of Pennsylvania and Peyton Young of Oxford university and the Brookings Institution, explain the point beautifully*. They start by asking us to consider a rare event – that the stock market will fall by 20 per cent over the next 12 months, for example. They assume, too, that the options market prices this risk correctly, say at one in 10. An option costs $0.1 and pays out $1.

Now imagine that we set up a hedge fund with $100m from investors on the normal terms of 2 per cent management fees and 20 per cent of the return above a benchmark. We put our $100m in Treasury bills yielding 4 per cent. We also sell 100m covered options on the event, which nets us $10m. We put this $10m, too, in Treasury bills, which allows us to sell another 10m options. This nets another $1m. Then we go on holiday.

There is a 90 per cent chance that this bet will pay off in the first year. The fund then grosses $11m on the sale of the options, plus 4 per cent interest on the $110m in Treasury bills, for a handsome 15.4 per cent return. Our investors are delighted. Assume our benchmark was 4 per cent. We then earn $2m in management fees, plus 20 per cent of $11.4m, which amounts to over $4m gross. Whatever subsequently happens, we need never give this money back.

The chances are nearly 60 per cent that the bad event will not occur over five years. Since the fund is compounding at a rate of 11.4 per cent a year after fees, we will make well over $20m even if no new money is attracted into this apparently stellar enterprise. In the long run, however, the bad event is highly likely to occur. Since we have made huge profits, our investors have paid us handsomely for the near certainty of losing them money.

The immediate response may be that so naked a scam is inconceivable. Well, imagine a fund that leverages investors’ money by borrowing massively in short-term money markets in order to purchase higher-yielding paper. Assume, again, that the premium gives a correct estimate of the risk. With sufficient leverage, this fund, too, is likely to make profits for years. But it is also very likely to be wiped out, at some point. Does this strategy sound familiar? It certainly should by now.

We can identify two huge problems to be solved. First, many investment strategies have the characteristics of a “Taleb distribution”, after Nicholas Taleb, author of Fooled by Randomness. At its simplest, a Taleb distribution has a high probability of a modest gain and a low probability of huge losses in any period.

Second, the systems of reward fail to align the interests of managers with those of investors. As a result, the former have an incentive to exploit such distributions for their own benefit.

Professors Foster and Young argue that it is extremely hard to resolve these difficulties. It is particularly difficult to know whether a manager is skilful rather than lucky. In their telling example, the chances are more than 10 per cent that the fund will run for 20 years without being exposed. In other words, even after 20 years the outside investor cannot be confident that the results were not being generated by luck or a scam.

It is also tricky to align the interests of managers with those of investors. Obvious possibilities include rewarding managers on the basis of final returns, forcing them to hold a sizeable equity stake or levying penalties for underperformance.

None of these solutions solves the problem of distinguishing luck from skill. The first also encourages managers to take sizeable risks when they are close to the return at which payouts begin. Managers can evade the effects of the second alternative by taking positions in derivatives, which may be hard to police. Finally, even under the apparently attractive final alternative it appears that any clawback contract harsh enough to keep unskilled managers away will also discourage skilled ones.

It is obviously best not to pay the manager, as a manager, at all, but rather to invest alongside him, as at Berkshire Hathaway, Warren Buffett’s investment company. But we still have the challenge of knowing whether the manager is any good. We know this today of Mr Buffett. Fifty years ago, that would have been very hard to know.

What we have then is a huge “lemons” problem: in this business it is really hard to distinguish talented managers from untalented ones. For this reason, the business is bound to attract the unscrupulous and unskilled, just as such people are attracted to dealing in used cars (which was the original example of a market in lemons). The lemons theorem states that such markets are likely to disappear. The same may happen to today’s hedge-fund industry.

Now consider the financial sector as a whole: it is, again, hard either to distinguish skill from luck or to align the interests of management, staff, shareholders and the public. It is in the interests of insiders to game the system by exploiting the returns from higher probability events. This means that businesses will suddenly blow up when the low probability disaster occurs, as happened spectacularly at Northern Rock and Bear Stearns.

Moreover, if these unfavourable events – stock market crashes, mortgage failures, liquidity freezes – come in stampeding herds (because so many managers copy one another), they will say: “Nobody could have expected this, but, now that it has happened to all of us the government must come to the rescue.”

The more one believes this is how an unregulated financial system operates, the more worried one has to become. Rescue from this crisis may be on the way, but what about next time and the time after next?

Friday, March 7, 2008

Fears of Recession from Employment Data

U.S. recession fears mounted Friday as employment fell in February at its fastest rate in five years, suggesting that the housing and credit crunch is gripping the broader economy.

The data further cemented Wall Street expectations for additional Federal Reserve rate cuts when officials meet in less than two weeks and in the months that follow. Financial markets even raised their already aggressive rate-cut forecasts in the wake of the report. * From WSJ.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}